Canadian tax system

Tax system in canada

In your journey as a newcomer to Canada, income taxes are typically not the

foremost concern. Understanding income taxes is crucial. We will provide essential information about the impact of taxes in Canada, the importance of timely tax payment. Understanding the intricacies of the Canadian tax system can still be challenging, despite the information provided on this page. Therefore, we recommend seeking assistance from a tax specialist when the time comes to file your income taxes.

Just like individuals, the Canadian government also earns income to cover its

expenses. This income comes from various taxes, including those on income,

corporations, capital gains, and sales. With this revenue, the government funds

projects like education, infrastructure, and social programs. The balance between

income and expenses is called the federal budget. If expenses exceed income in a

given year, it results in a budget deficit. Conversely, if income surpasses expenses,

there is a surplus. In case of a deficit, the government borrows money by issuing T-Bills, which are essentially IOU notes promising repayment in the future. To reduce debt, the government often needs to increase income, typically through higher taxes. Personal

income taxes are a significant part of the government’s revenue, accounting for

40.8% of federal income at their peak in 1990. The following section explores the

history of personal income tax changes in Canada in relation to the federal budget.

Personal income Tax

Canadian residents are taxed on their global income, with provisions for relief from

double taxation via international tax treaties and foreign tax credits.

Non-residents pay taxes on Canadian employment income, business earnings, and

capital gains from taxable Canadian property.

Part-year residents are taxed on their worldwide income for the period of residency.

Various tax credits are deducted from the federal tax liability calculation.

You have several ways to do your taxes, including options that are free or have

varying costs, or others where you are invited by the CRA.

Choose a filing option:

1) Certified tax software (electronic filing)

Use CRA-approved tax software to calculate and file your taxes electronically.

Options include online, downloaded, or installed on your computer, mobile, or tablet.

-Who can use: Canadian residents

-Cost: Free or can vary

-Processing time: Typically, within 2 weeks

2) Authorize a representative.

Authorize a family member, friend, or an accountant to act on your behalf to

complete your taxes and access your tax accounts.

-Who can use: Anyone.

-Cost: Free or can vary

-Processing time: Usually, in a span of 2 weeks.

3) Community volunteer tax clinic

Find a free tax clinic to have a volunteer complete your taxes for you.

-Who can use: People with a modest income, and a simple tax situation.

-Cost: Free

-Processing time: Usually, in a span of 2 weeks.

4) Discounter (tax preparer)

A discounter is a tax preparer who calculates your refund and pays you a discounted

tax refund right away, before they file your tax return.

-Who can use: Anyone.

-Cost: Can vary

-Processing time: Discounted refund is paid by the tax preparer right away.

5) Paper tax return

Complete and file your taxes manually on a paper return.

-Who can use: Anyone.

-Cost: Free

-Processing time: 8 weeks if filed on time.

Eligible individuals will receive an invitation letter from the CRA. To submit your

taxes, input your details via the automated phone service.

-Eligibility: Invited individuals with low or fixed income and uncomplicated tax

scenarios.

-Cost: No charge.

-Processing Time: Typically processed within 2 weeks.

2) Tax Filing Assistance from a CRA Agent:

You can complete and file your taxes over the phone with the assistance of a CRA

agent. Eligible individuals will receive an invitation via mail or My Account.

-Eligibility: Invited individuals with modest income and straightforward tax

situations.

-Cost: No charge.

-Processing Time: Typically processed within 2 weeks.

Personal income tax rates

– Quebec has its unique personal tax system, requiring a separate calculation of

taxable income. Given that Quebec administers its own tax collection, federal income

tax is reduced by 16.5% of the basic federal tax for Quebec residents.

– Non-residents, instead of provincial or territorial tax, pay an additional 48% of the

basic federal tax on income taxable in Canada but not earned in a province or

territory. Non-residents are subject to provincial or territorial rates on employment

income earned and business income related to a permanent establishment (PE) in

the respective province or territory. Different rates may apply to non-residents in

other situations.

– The combined federal/provincial (or federal/territorial) effective top marginal tax

rates for 2023 are presented below. These rates encompass all 2023 federal,

provincial, and territorial budgets, typically introduced each spring. They include all

provincial/territorial surtaxes and apply to taxable incomes above CAD 235,675 in all

jurisdictions, except for:

– CAD 341,502 in Alberta.

– CAD 240,716 in British Columbia.

– CAD 1,059,000 in Newfoundland and Labrador.

– CAD 500,000 in Yukon.

In Canada, there are two dividend categories: “Eligible Dividends” and “Other Than

Eligible Dividends.” Corporations classify their dividends as either “eligible” or “other

than eligible” for taxation purposes.

Dividends are distributed from a corporation’s post-tax earnings, meaning that taxes

have already been paid on the dividend sum. However, not all corporations are

subject to the same tax rate.

Canadian Controlled Private Corporations (CCPCs) are entitled to the small

business deduction, reducing their corporate income tax rate. Consequently,

dividends paid by CCPCs fall into the “other than eligible” category. Because a lower

amount of tax has been paid on them, you’ll receive a smaller tax credit.

Public corporations, on the other hand, are not eligible for the small business

deduction. Therefore, their dividends are categorized as eligible dividends. Given the

higher tax rate applied to these public corporations, your dividend tax credit will be

greater.

A dividend gross-up multiplies your actual dividend amount by a specific factor,

aiming to replicate what the dividend-paying corporation needed to earn to pay out

the dividend after taxes.

College programs vary in length, often making them more affordable than university

studies. Some programs include work-integrated learning, which may provide an

income while you’re in Canada.

High-quality colleges and vocational schools are found across Canada, including

smaller cities and towns with lower living costs. Even larger Canadian cities are

relatively more affordable than many cities worldwide.

Tuition fees for international students in Canada vary based on the program and

location you select.

Canada also boasts independent and private secondary schools that charge tuition

fees. These private institutions must adhere to the same curriculum as public

schools in their respective province or territory, ensuring that students receive an

equivalent education.

Private school classes are often smaller than those in public schools, affording

students the opportunity to benefit from specialized programs. Some private schools

incorporate religious education alongside standard subjects, and there are

institutions catering exclusively to boys or girls.

Private high schools encompass boarding schools with on-site accommodations,

alternative schools, International Baccalaureate programs, and specialized sports

schools or schools tailored to students with unique learning requirements.

Provincial/territorial income taxes

Apart from federal income tax, individuals residing in or earning income in a province or territory are also subject to provincial or territorial income tax. In all regions except Quebec, these taxes are calculated through the federal return and collected by the federal government. Tax rates vary among provinces and territories, with two provinces imposing surtaxes that can increase the provincial income tax owed. It’s important to note that provincial and territorial taxes cannot be deducted when calculating federal, provincial, or territorial taxable income. All provinces and territories use a ‘tax-on-income’ system, where they establish their own rates, brackets, and credits. Except for Quebec, they follow the federal definition of taxable income.

Sources of Revenue in Canada

Nations generate their tax revenue using a combination of individual income taxes, corporate income taxes, social insurance taxes, taxes on goods and services, and property taxes. The specific blend of tax policies can impact whether a tax system is

distortionary or neutral. Taxes on income can potentially cause more economic disruption compared to taxes on consumption and property. Nonetheless, the degree to which a country depends on any of these tax types can greatly vary.

Corporate income tax is a tax on corporate profits, and it varies among OECD

countries. It’s considered detrimental to economic growth, but lower tax rates and

substantial capital allowances can mitigate its impact.

Capital allowances affect business incentives for new investments by allowing

businesses to deduct the cost of investments over several years rather than

immediately. More generous capital allowances in a country’s tax system can boost

business investment and promote economic growth.

Individual income taxes are a common way for OECD countries to generate

government revenue. These taxes are progressive, meaning higher earners pay a

higher tax rate.

Countries also have flat-rate payroll taxes on wage income, separate from individual

income tax. The revenue from these taxes often goes to social insurance programs

like unemployment, pensions, and health insurance.

High marginal tax rates can influence work decisions and tax system efficiency.

Capital gains and dividend income may be taxed at a flat rate if not covered by

individual income tax.

Consumption taxes, like VAT, are common worldwide. They usually avoid taxing

business inputs to prevent tax pyramiding, making them efficient for raising revenue.

But some countries wrongly define their tax base by exempting too much or applying

reduced rates, requiring higher standard rates. Some also fail to exempt business

inputs, like machinery and equipment in some U.S. states.

Property taxes are levied on assets of individuals or businesses. Estate and

inheritance taxes apply upon an individual’s death or the transfer of their estate to an

heir. Meanwhile, taxes on real property, like land and houses, are typically paid at

regular intervals, often annually.

Many property taxes are complex and can negatively impact taxpayers and

businesses. Estate and inheritance taxes discourage work and saving, hindering

productivity. Financial transaction taxes raise capital costs, limiting efficient

investments. Wealth taxes reduce available capital, harming economic growth and

innovation.

Effective tax policy aims to minimize economic distortions. However, apart from land

taxes, most property taxes create economic distortions and have long-term adverse

effects on an economy and its productivity.

In the globalized economy, businesses expand globally, leading to the need for

international tax rules that govern corporate income earned abroad. Tax treaties

align tax laws between countries to prevent double taxation, making countries with

extensive treaty networks more appealing for foreign investment and competitive.

The Future of Tax in Canada

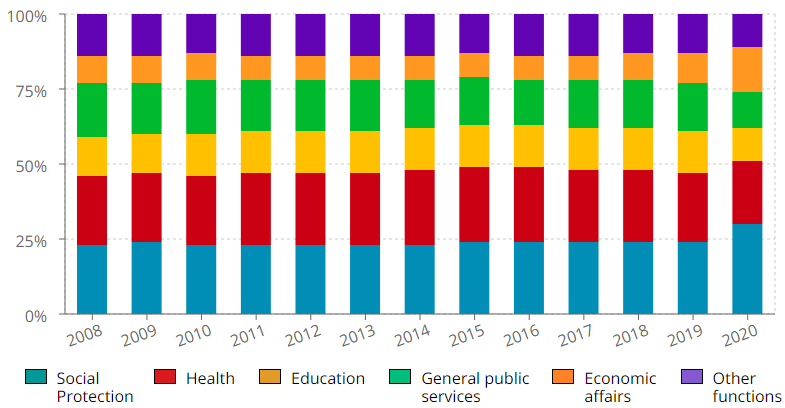

The category “other functions” includes defence, public order and safety, environmental protection, housing and community amenities, as well as recreation, culture, and religion.

Governments continually seek ways to boost revenue, which may involve tax hikes, or they can achieve budget surpluses by trimming expenses. As the Baby Boomer generation retires, the government must explore cost-cutting measures due to a shrinking workforce and tax base. One strategy might involve increasing the retirement age. Another approach could entail revising eligibility criteria for specific programs like Old Age Security or Employment Insurance. Additionally, the government might consider reducing tax credits or deductions. Regardless of the government’s future tax changes, it’s crucial to recognize that taxes play a vital role in funding essential services like education, healthcare, and infrastructure.

The elected government plays a significant role in determining how tax payments are

distributed. When Prime Minister candidates’ campaign, they often outline their plans

for tax revenue allocation during their term. This section will elucidate the spending

priorities of Canada’s major political parties.

Categorized Federal Government Spending (From 2008 to 2020)

Relocate to Canada Today!

Complete our online registration to be evaluated and we will provide our assessment within 2-3 business days.